Why Telegram ASIC Deals Still End in Dispute (And What Bitcoin Escrow Fixes)

The used ASIC market runs on Telegram, where reference checks and screenshots fail predictably. Bitcoin-native 2-of-3 multisig escrow locks payment until both parties agree, or a court orders release. No inspection, no arbitration, no custody.

The secondary ASIC market has exploded. Public miners are liquidating fleets of twenty thousand to one hundred thousand machines as they pivot to AI infrastructure. Second-hand units trade at forty to sixty percent of new price, with immediate availability that Bitmain's twelve-week lead times cannot match. The bottleneck is no longer supply or price: it is trust. And the channel where most of this volume transacts — Telegram — was never built for it.

This article explains how used ASIC deals actually get done today, why the current trust mechanisms fail predictably, and where Bitcoin-native, non-custodial escrow fits into a workflow that is already Telegram-native.

1) The market context: why Telegram is the exchange

If you want to buy used S19s or S21s in bulk, you do not start with a website. You start with a Telegram channel. Kaboomracks, ASIC Solutions Marketplace, Hardware Market, and dozens of smaller operators run their entire sales pipeline through Telegram: listings go to the channel, negotiation moves to direct messages, and payment settles by wire transfer, Zelle, or cryptocurrency.

Chris McIntyre, who has written extensively on how to source mining hardware, puts it plainly: "Most of the communication regarding ASICs takes place through Telegram but I don't recommend purchasing if you can't get the supplier on the phone." That sentence captures the entire market. The infrastructure is a messaging app. The due diligence is a phone call. The settlement is whatever the two parties agree to.

This is not a criticism of Telegram. It is an observation that a global, multi-billion-dollar secondary market for high-value capital equipment has coalesced around a platform with no native payment protection, no identity verification, and no transaction enforcement. Buyers and sellers make it work with references, screenshots of past deals, and accumulated reputation. Until it stops working.

2) How a Telegram ASIC deal actually works

The typical sequence looks like this:

- Discovery: Buyer joins a Telegram channel (e.g., Kaboomracks Marketplace) and reviews pinned listings for available lots.

- Inquiry: Buyer forwards the listing to the channel admin or broker and requests availability.

- Negotiation: Terms — price, quantity, shipping method, payment method — are negotiated via direct message.

- Due diligence: Buyer asks for references. Seller provides screenshots of past deals or names of prior buyers who can "vouch."

- Payment: Depending on the deal size and relationship, buyer may send a downpayment (thirty to fifty percent) by wire, Zelle, or cryptocurrency, with the balance due before shipping.

- Shipping: Seller arranges freight and provides tracking.

- Acceptance: Buyer receives the units, tests them, and either accepts or disputes.

In the best case, steps four through seven happen on trust established by step four. In the worst case, the buyer wires fifty thousand dollars to a seller who disappears, ships misrepresented units, or delivers nothing at all.

The critical gap is between payment and delivery. In most Telegram deals, that gap is bridged by nothing more than a reference check and a hope.

3) Why references and reputation fail at scale

References work when the market is small and incestuous enough that a bad actor is ostracized. The used ASIC market is no longer small. Public miner liquidations have injected enormous inventory into the secondary channel, and new buyers enter daily who cannot distinguish a three-year broker from a three-day scammer.

HashFloor, a market intelligence platform for mining hardware, built its brand around the exact problem: "Stop relying on Telegram hearsay — make data-driven hardware decisions." The phrase is telling. "Hearsay" is the state of the art for price discovery and seller verification in the largest secondary market for Bitcoin mining equipment.

References fail for specific reasons:

- Collusion: The "reference" is the seller's own alternate account or a paid accomplice.

- Stale reputation: A legitimate operator with two years of clean deals faces financial pressure, ships a bad lot, and disappears.

- Impersonation: A scammer copies the name, photo, and username format of a known seller and intercepts inbound buyers.

- Scale mismatch: A seller who reliably moved ten-unit hobbyist deals is suddenly brokering a five-hundred-unit institutional transaction with no operational capacity to fulfill.

None of these are rare edge cases. They are standard failure modes in a marketplace where identity is a username and reputation is a screenshot.

4) The specific scams that exploit Telegram's trust gap

Understanding the mechanics matters because each scam has a specific structural weakness that escrow either prevents or does not. Here are the dominant patterns.

The bogus escrow

A buyer who is not comfortable wiring funds first asks to use escrow. The seller agrees and recommends an escrow service the buyer has never heard of. The site looks professional. It displays logos from the Better Business Bureau, TRUSTe, and VeriSign. The buyer sends funds. The escrow service — which is a shell operation or a copied template — disappears.

This is a well-documented confidence trick. Wikipedia catalogs it as "bogus escrow": a scammer operates a fake escrow service, collects the buyer's funds, and vanishes. The California Department of Financial Protection and Innovation notes that when fraudulent escrow sites are detected and shut down, scammers copy the defunct site's files, register a new domain, and are "quickly back in business."

In the Telegram ASIC market specifically, buyers have reported channels like @asichardware purporting to offer escrow services, only to be flagged by the community as fraudulent. One Reddit user in r/ASICMinersTalk asked about the channel's legitimacy and received the blunt response: "It's a scam."

The impersonation trap

A scammer joins the same Telegram channel as a legitimate seller, copies the seller's display name and profile photo, and waits. When a buyer messages the "seller" to inquire about a listing, the scammer — not the real seller — responds. The buyer thinks they are negotiating with a known broker. They are negotiating with a facsimile.

Reddit users have documented this pattern repeatedly. In one case, a buyer was approached by an individual impersonating a group's admin, claiming escrow was unnecessary for their direct deal. The buyer lost their downpayment. The real admin had nothing to do with it.

The downpayment harvest

A seller — or someone posing as one — advertises miners at an attractive price. When the buyer hesitates at prepaying in full, the seller offers a "compromise": a thirty to fifty percent downpayment, with the balance due on shipping. The buyer sends the downpayment. The seller disappears. The downpayment is cheaper than the full amount, but it is still gone.

The "Valley ASIC Mining Club" scam, documented on Reddit, followed this exact playbook. The operator promoted miners for sale, offered downpayment terms to build trust, and collected partial payments from multiple buyers before vanishing.

The fake vouch system

In Telegram channels where buyers and sellers post "vouches" (testimonials of completed deals), the vouch itself becomes the attack surface. Scammers create multiple accounts, stage fake transactions between them, and post glowing vouches. A buyer who checks references sees five or ten positive testimonials and assumes the seller is established. The testimonials are self-generated.

5) What does not fix the problem

Not every solution marketed as "secure" actually reduces risk. Here are the approaches that sound right but do not work structurally.

Telegram escrow bots

Various bots on Telegram claim to hold funds in escrow during a transaction. The problem is opacity. The buyer sends cryptocurrency to a bot address with no visibility into who controls the private keys, how release decisions are made, or whether the bot is even a multi-party construct rather than a single operator's wallet. One Reddit user asked about @coinescrowbot and received no verifiable information about its legitimacy or structure. Trusting an un-audited Telegram bot with a six-figure ASIC payment replaces one opaque counterparty with another.

"I know a guy" middlemen

Brokers who position themselves as trusted intermediaries can help match buyers and sellers, but if the broker also handles payment collection, the situation degrades into custodial risk. The buyer is no longer trusting the seller; they are trusting the broker not to abscond. If the broker's incentive structure is a flat fee, there is limited reason to defect. If the broker is under financial pressure, the incentive changes. This is not a theoretical concern — brokers in distressed markets have incentive to keep funds flowing through their accounts regardless of deal outcomes.

Verbal agreements and "standard terms"

In Telegram negotiations, terms are often informal: "Payment first, then ships," or "Fifty percent now, fifty percent on tracking." When a dispute arises, there is no written contract, no agreed evidence standard, and no neutral arbiter. Each side tells their story to the Telegram group chat, and public opinion — manipulated by fake accounts and vested interests — becomes the court.

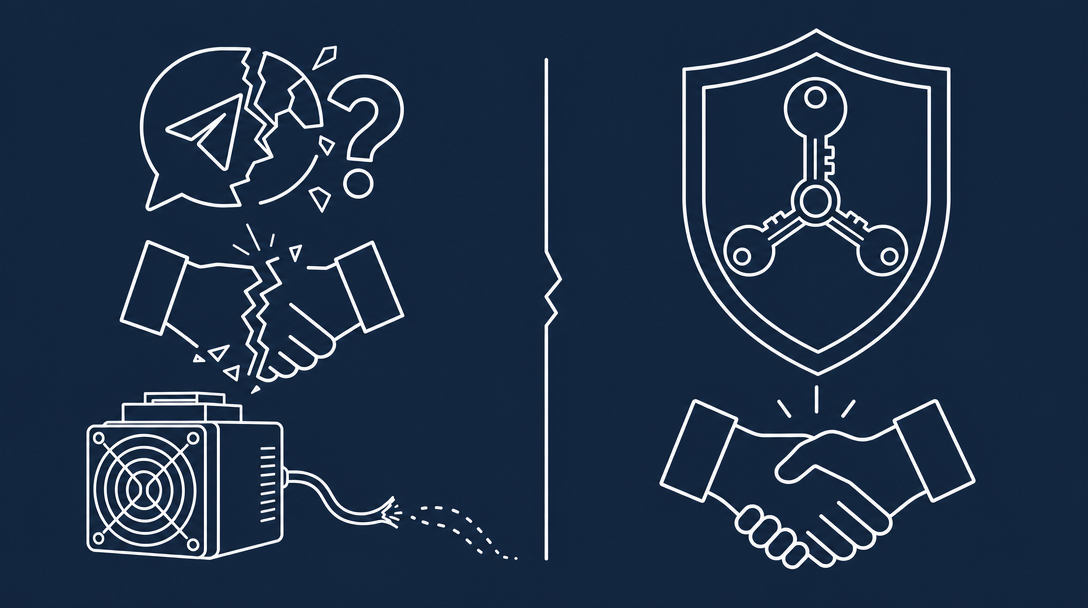

6) What Bitcoin-native escrow actually fixes

The clean model is the same one described in our prior article on ASIC escrow: a 2-of-3 multisig arrangement where the buyer holds one key, the seller holds one key, and a neutral coordinator holds one key. Funds can move only with two signatures. If the deal concludes smoothly, the coordinator never touches the money.

This architecture solves structural problems that Telegram's trust-based model cannot.

The coordinator cannot steal the funds

In a bogus escrow scam, the fake escrow service is the only party who can move the money. In a 2-of-3 multisig, the coordinator cannot unilaterally spend. Even if the coordinator is compromised or malicious, they cannot release funds to themselves without colluding with either the buyer or the seller. The threat model shifts from "trust the escrow agent" to "trust that the escrow agent cannot act alone."

The escrow address is verifiable before any payment

Before the buyer sends a single satoshi, all three parties can independently verify the multisig address and the wallet configuration. This eliminates the substitution attack where a scammer provides a deposit address they control. If the address derivation does not match the agreed-upon configuration — visible to all parties — the deal does not proceed.

The terms are locked before payment

A well-run multisig escrow forces the parties to agree on terms before funding: exact unit list, acceptance criteria, shipping method, and inspection window. These terms matter because they define what each party promised, but they do not give the coordinator authority to judge whether those terms were met. The coordinator does not inspect hashboards, evaluate unboxing videos, or decide who is right in a disagreement. The coordinator holds the third key and will only cosign a transaction when both parties agree, or when directed to do so by a court.

Release requires agreement or a court order

Funds move when the buyer and seller both sign a release. If the deal concludes smoothly, the coordinator is never needed. If a dispute arises, the coordinator does not arbitrate. The bitcoin remains locked in the multisig address until the parties resolve the matter between themselves, or one party obtains a court order directing the coordinator to release the funds to a specific address. This is not a limitation of the service — it is the design. The coordinator provides cryptographic neutrality, not subjective judgment.

7) How Bitcoin escrow fits into a Telegram-native workflow

The objection is obvious: ASIC buyers and sellers live on Telegram. They are not going to migrate to a separate platform for every transaction. The answer is that they do not have to.

A Bitcoin-native escrow coordinator can operate within the existing Telegram workflow:

- Deal initiation: Buyer and seller agree on terms in Telegram DMs, same as always.

- Escrow setup: Both parties engage the coordinator, who provides a wallet configuration and verified multisig address.

- Funding: Buyer deposits bitcoin into the multisig address. The transaction is visible on-chain.

- Shipping: Seller ships the hardware, providing tracking.

- Acceptance: Buyer verifies the units against the agreed terms.

- Release: Both parties sign the release transaction. Funds settle to the seller instantly.

The coordinator's role is lightweight: provide the multisig infrastructure, hold the third key, and cosign only upon mutual agreement or court order. The buyer and seller remain in control. Telegram remains the communication layer. Bitcoin becomes the trust layer.

8) What multisig escrow does not prevent

It is important to be honest about limitations. Bitcoin escrow does not solve problems outside its scope.

- Bait-and-switch units: Escrow does not inspect hashboards. The buyer still needs to verify the units on arrival.

- Transit damage: If a carrier damages the shipment, escrow cannot determine fault between the seller's packing and the carrier's handling.

- Market timing: If the buyer's financing falls through after funding escrow, the bitcoin is locked until the seller agrees to a refund or the coordinator rules.

Escrow makes one thing reliable: the payment cannot move unless both parties agree, or a court orders it. It does not make the hardware reliable. Buyers still need acceptance criteria, unboxing evidence, and the discipline to test before signing a release.

9) Red flags that should make any buyer pause

Regardless of whether escrow is used, certain patterns are strong predictors of fraud:

- A seller who insists on a specific, unknown escrow service. The seller's incentive to recommend a particular escrow provider should be treated with the same skepticism as a seller who insists on a particular payment method.

- Pressure to skip escrow for "speed" or because "we've done this before." Speed is the enemy of verification in high-value physical goods transactions.

- Screenshots as the only proof of legitimacy. Screenshots can be fabricated, staged, or taken out of context. On-chain transaction history is harder to fake.

- A deal that feels "too good" relative to HashFloor or MiningWatchdog pricing. Significant discounts to market are either distressed inventory (which exists, but rarely) or a lure.

- Communication that shifts from the public channel to an alternate username mid-negotiation. This is the impersonation pattern in action.

10) The practical path forward

The used ASIC market is not going to abandon Telegram. It is fast, global, and already where the liquidity lives. But the market can add a settlement layer that does not depend on references, screenshots, and hope.

For buyers: demand structurally secure settlement. If a seller will not use verifiable, non-custodial escrow, ask yourself what they gain from avoiding it.

For sellers: escrow is not an accusation of distrust. It is a tool that lets you close deals with buyers who would otherwise walk away. The seller who offers verifiable escrow as standard closes more deals, faster, with less negotiation friction.

For the market: every failed deal — every bogus escrow, every impersonation scam, every disputed wire — adds friction that makes the secondary market less liquid. A reliable settlement layer benefits legitimate buyers and sellers equally by making trust computable instead of performative.

The Telegram marketplace is not going anywhere. Neither is the need to settle with finality.

References

- Blockspace / Yahoo Finance. "Public Miners Are Selling Thousands of ASICs Amid AI Pivots." blockspace.media/insight/the-great-asic-sell-off-public-miners-liquidate-thousands-of-rigs/ and finance.yahoo.com/markets/crypto/articles/great-asic-sell-off-public-191141312.html

- CoinShares. "Bitcoin Mining Report — Q1 2026." coinshares.com/corp/insights/research-data/bitcoin-mining-report-q1-2026/

- McIntyre, Chris. "How to Buy ASICs." LinkedIn / Medium. linkedin.com/pulse/how-buy-asics-chris-mcintyre and chrispmac.medium.com/how-to-buy-asics-3b2457cabfe2

- HashFloor. "The Source of Truth for Mining Hardware." hashfloor.com

- Kaboomracks Marketplace (Telegram). t.me/s/kaboomracksmarketplace

- D-Central. "How to Spot a Scam when Buying ASIC Miners Online." d-central.tech/how-to-spot-a-scam-when-buying-asic-miners-online/

- Wikipedia. "Bogus escrow." en.wikipedia.org/wiki/Bogus_escrow

- California Department of Financial Protection and Innovation. "Online Escrow Fraud Questions & Answers." dfpi.ca.gov/regulated-industries/escrow-law/online-escrow-companies/online-escrow-fraud-questions-answers/

- r/ASICMinersTalk. "Has anyone used Telegram Channel asichardware for escrow?" reddit.com/r/ASICMinersTalk/comments/1ioaf6k/

- r/cryptomining. "Valley Asic Mining Club — telegram scam and awareness." reddit.com/r/cryptomining/comments/1cgx1tb/

- MiningWatchdog Marketplace. marketplace.miningwatchdog.com

- ASIClist.com. "How to Buy Used ASIC Miners Safely: A Practical Guide." asiclist.com/insights/how-to-buy-used-asic-miners-safely